What is tokenization? How it works and why it matters in payments

Every time a customer pays online, sensitive data is involved: card numbers, expiration dates, and security codes. If that data is exposed, the consequences can be costly for both your business and customers.

That’s where tokenization comes in.

Tokenization is one of the most important security technologies in payments. It allows you to accept and process payments without ever storing or exposing real card details, reducing fraud risk, simplifying compliance, and improving the customer experience at checkout.

Whether you're running an e-commerce store, managing subscriptions, or handling payments across multiple channels, this payment technology plays a key role in keeping transactions secure and seamless.

In this article, you’ll learn:

- What is payment tokenization?

- What is a token in payments?

- How payment tokenization works

- Benefits of tokenization for businesses

- Tokenization vs encryption

- Common use cases for tokenization in payments

- Tokenization at MONEI

What is payment tokenization?

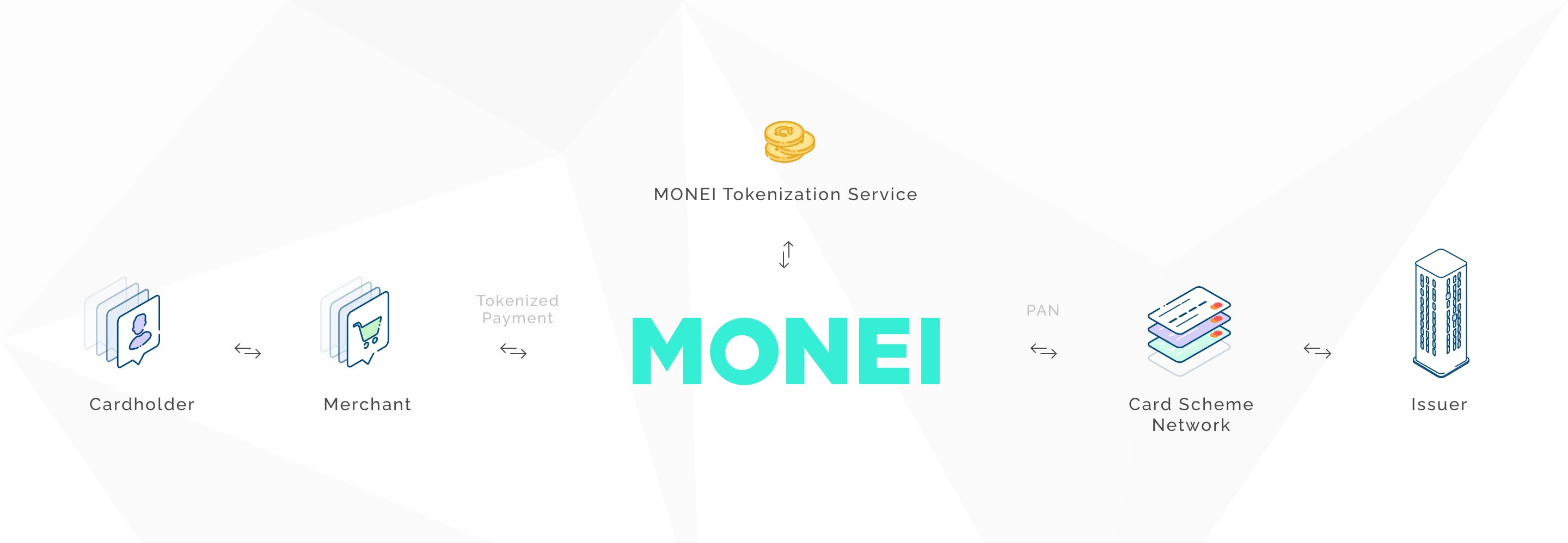

It is a payment security process that replaces sensitive data — like a customer’s Primary Account Number (PAN) or card number — with a unique, randomly generated value called a token.

The token acts as a secure reference to the original data, which is stored separately in a protected system (often called a token vault) managed by a payment service provider (PSP). On its own, the token has no value and can’t be used outside that specific payment environment.

Instead of handling real card details, your business only stores and processes tokens, significantly reducing its exposure to sensitive data.

In simple terms:

- Card details are replaced with a token

- Businesses store the token, not the card data

- Only the payment provider can map the token back to the original data

This approach reduces the risk of data breaches without adding friction to the payment experience.

Tokenization is used across payment flows, including:

- Online checkouts

- Saved cards and one-click payments

- Recurring billing and subscriptions

- Digital wallets like Apple Pay or Google Pay

Payment tokenization vs network tokenization

Payment tokenization involves a payment service provider (like MONEI) retaining a customer's card details, like the PAN, Primary Account Number (PAN), and creating tokens. These tokens are then used by merchants for processing payment transactions.

Network tokenization, on the other hand, is handled by card networks such as Mastercard, Visa, and American Express. In this scenario, these networks store the PAN and are responsible for token generation. A key advantage is that the tokens remain current and valid, even if the original card details change or expire, because the card networks manage the entire process from start to finish.

Payment tokenization vs credential on file (COF)

Payment tokenization replaces sensitive card details, while Credential on file (COF) refers to the practice of securely storing a customer’s payment details — either as raw card data or, more commonly, as a token — for future transactions. These can include one-click payments, subscriptions, or merchant-initiated charges.

What is a token in payments?

A token is a randomly generated string of characters that replaces sensitive payment data, such as a credit card number. It acts as a secure reference to the original data, but unlike the real card details, it has no intrinsic value and cannot be reverse-engineered or used outside the system that created it.

Key characteristics of a token:

- No usable value. If a token is stolen, it can’t be used to complete a transaction.

- System-specific. A token only works within the payment environment it was created for.

- Format-preserving (in some cases). Tokens may look like card numbers, but they don’t contain real data.

Reusable (depending on type). Some tokens can be used for future payments, like subscriptions or saved cards.

How payment tokenization works

The process happens behind the scenes in seconds, with no added friction for the customer — the payment experience feels exactly the same.

Here’s how the process works step by step:

- The customer enters their payment details. At checkout, the customer provides their card information through a secure payment form.

- The payment provider captures the data securely. The payment provider (or gateway) collects the sensitive data and sends it to a secure environment designed for tokenization.

- The data is replaced with a token. The provider generates a unique token that represents the card details. This token has no connection to the original data outside the provider’s system.

- The token is returned to the business. The business receives the token and stores it instead of the actual card data.

- The token is used to process the payment. When the transaction is processed, the token is sent through the payment network. The provider securely maps it back to the original card details to complete the transaction.

- The token can be reused (if applicable). For recurring payments or saved cards, the same token can be used again — without requiring the customer to re-enter their details.

Since your business never handles raw card data, the risk of exposing sensitive information is reduced. Even in the event of a breach, tokens are essentially useless to attackers.

At the same time, tokenization enables faster, smoother payment experiences — like one-click checkout and automatic billing — without compromising security.

Benefits of tokenization for businesses

According to a Nasdaq report, 8 out of 10 Spanish consumers experienced scam attempts in 2024. Tokenization is one way to reduce this by protecting payment data. It improves how your business handles payments, making transactions more secure, efficient, and scalable.

- Stronger payment security. Ir reduces the risk of fraud by replacing sensitive card data with tokens that have no usable value. Even if a token is intercepted, it can’t be used to complete a transaction or access the original card details.

- Lower risk in case of data breaches. Because your business doesn’t store raw card data, your exposure is significantly reduced. In the event of a breach, attackers won’t gain access to sensitive payment information — helping protect your customers and your reputation.

- Easier PCI DSS compliance. It helps reduce the scope of PCI DSS requirements by limiting the amount of sensitive data your systems handle. While it doesn’t eliminate PCI compliance obligations, it makes them more manageable and lowers your operational burden.

- Better customer experience. With tokenization, customers don’t need to re-enter their card details for every purchase. This enables faster checkouts, one-click payments, and a smoother overall experience — especially for returning customers.

- Supports modern payment use cases. It powers many of the payment experiences customers expect today, including:

- Saved cards and one-click checkout

- Recurring billing and subscriptions

- Digital wallets like Apple Pay and Google Pay

- Omnichannel payments across online and in-store channels

Tokenization vs encryption

These two payment technologies are often used together to reduce the amount of sensitive data stored in the first place (tokenization) and to protect data while it’s being transmitted (encryption).

Tokenization replaces sensitive data with a completely different value (a token). The original data is stored securely in a separate system (a token vault), and the token has no mathematical relationship to the original data.

- No sensitive data is exposed or stored by the business

- Tokens are useless if intercepted

- Only the payment provider can map the token back to the original data

Encryption transforms sensitive data into an unreadable format using a cryptographic key. The data can be decrypted back to its original form, but only with the correct key.

- Protects data in transit and at rest

- Encrypted data can be reversed with the right key

- Businesses may still handle encrypted sensitive data

Common use cases for tokenization in payments

Tokenization powers many of the payment experiences customers expect today, often without them even realizing it. It’s especially valuable if your business stores, reuses, or processes payment data across channels. Here are the most common use cases:

Saved cards and one-click checkout

For e-commerce businesses, this process allows you to store a secure token instead of the customer’s card details. This enables faster repeat purchases and reduces friction at checkout.

Recurring payments and subscriptions

Subscription and SaaS companies use tokenization to charge customers automatically without storing sensitive data. Once a token is created, it can be reused securely for future billing cycles.

Digital wallets

Payment methods like Apple Pay, Google Pay, and Click to Pay rely on tokenization to securely store and transmit card details. Customers can complete purchases quickly without sharing their actual card information.

Omnichannel payments

If your business operates both online and in-store, use tokenization to unify payment data across channels. A customer’s payment method can be securely reused across websites, physical stores, and mobile apps.

Platforms and marketplaces

Platforms that manage payments between multiple parties use tokenization to securely handle payment data at scale. It enables recurring payouts, flexible payment flows, and reduced exposure to sensitive information.

Tokenization at MONEI

With MONEI, tokenization is built into your payment infrastructure, so you can accept, store, and reuse payment details securely without handling sensitive data directly.

When a customer makes a payment, our payment gateway replaces their card details with a secure token. Your business only interacts with that token, while the original data is safely stored and managed within our PCI-compliant environment.

What you can do with tokenization at MONEI:

- Accept payments securely. Process transactions without exposing or storing raw card data.

- Enable saved payment methods. Let returning customers pay faster using securely stored tokens.

- Support recurring billing. Use tokens to charge customers automatically for subscriptions or repeat purchases.

- Offer digital wallets. Accept Apple Pay, Google Pay, and other tokenized payment methods with built-in security.

- Unify payments across channels. Use the same tokenized data across online, in-store, and mobile payment flows.

One-time and reusable tokens

MONEI supports different token types depending on your use case:

- One-time tokens are used to securely process a single transaction.

- Reusable tokens allow you to store a customer’s payment method and use it again for future payments, such as subscriptions or one-click checkout.

We’re here to handle tokenization for you, so you can reduce your business's exposure to sensitive data, simplify compliance, grow your sales faster, and provide frictionless customer payment experiences.

You may also like to read:

- What is a Payment Gateway? Why You Need One & How it Works

- PSD2: What is It? Why it’s Important + How to Be Compliant

- What is SCA? (+ How it Benefits Consumers)

- The Top 4 Digital Wallets to Add to Your Online Store + Benefits for E-commerce

- AI in Payments: How It’s Transforming the Industry

🎓Find more definitions in our payment industry glossary.

Check all of MONEI's payment security measures.

Tokenization FAQ

What is tokenization in the context of e-commerce?

Tokenization in e-commerce refers to the process of replacing sensitive payment card data, like credit card numbers, with a unique identifier called a token. This token can be used for transaction processing, while the actual card details are securely stored by a payment service provider or a tokenization service.

Is tokenization compliant with PCI DSS?

Yes, it helps you achieve PCI DSS compliance. By eliminating the storage of sensitive card data, you can significantly reduce the scope of your PCI audit, as the tokenization service provider bears the responsibility of safeguarding the actual card information.

Can tokens be reversed to retrieve the original payment card details?

No, they are irreversible. They are generated using mathematical algorithms that cannot be reversed to retrieve the original card information. Tokens are designed to be used as substitutes for card data without exposing sensitive details.

Are tokens unique to each merchant or shared across multiple merchants?

Tokens are unique to each merchant. The tokenization process generates a token specific to your environment and system, so nobody else can use it.

Can tokens be used for multiple transactions?

Yes, tokens can be used for multiple transactions within the same system. Once a payment card is tokenized, the token can be securely stored for future use, such as processing recurring payments or facilitating a seamless checkout experience for returning customers.

What happens if a tokenized transaction needs to be refunded?

When a refund is requested, you need to use the token to identify the original transaction and initiate the refund process. The payment service provider matches the token with the actual card details in their secure storage, processes the refund, and communicates the outcome back to you.

How secure is tokenization compared to other payment security methods?

Tokenization is considered a highly secure payment method for protecting cardholder data. It minimizes the risk of data breaches, as tokens hold no value for attackers without the associated card details. Compared to other methods like data encryption, it offers an added layer of security.

Does tokenization affect the customer's payment experience?

It generally improves the customer's payment experience. Once the card is tokenized, customers can make future purchases without repeatedly entering their card details. This convenience speeds up the checkout process and reduces friction for returning customers.

How can I implement tokenization in my e-commerce store

To implement tokenization, you can integrate with a payment service provider (like MONEI) that supports your e-commerce platform. It will provide you with the necessary APIs and documentation to securely tokenize and store payment card data.

Is tokenization applicable to all types of payment methods, such as debit cards and digital wallets?

Yes, it can be used for various payment methods, including credit cards, debit cards, and digital wallets. The process replaces the sensitive card data with tokens, regardless of the payment method used by the customer.

Is tokenization used for in-store transactions as well, or is it limited to online payments?

It can be used for both online and in-store transactions. Many payment service providers offer solutions that support tokenization across various sales channels, including online, in store, and mobile payments.

Are there any additional costs associated with implementing tokenization?

There may be costs associated with implementing tokenization depending on the PSP you use, but not with MONEI. We charge transaction fees, but you won’t incur additional fees for using this technology.

Can tokens expire or become invalid over time?

Tokens can be configured with an expiration period if required. However, the expiration of tokens is typically managed by the payment service provider, and you would need to check their specific tokenization guidelines to understand the lifespan of tokens in your system.

What happens if there is a breach in the tokenized data?

In the event of a breach, tokenized data alone is useless to attackers since it does not contain the original card details. However, it’s still essential to follow payment security best practices and to regularly monitor for any signs of unauthorized access or suspicious activity

Are there any legal or regulatory considerations when implementing tokenization?

While tokenization can enhance security and compliance, it's important to consult with legal experts and understand the specific laws and regulations governing your industry and jurisdiction. Compliance requirements such as GDPR or data privacy laws may have implications for how tokenization should be implemented and managed.

Alexis Damen

Alexis Damen is a former Shopify merchant turned content marketer. Here, she breaks down complex topics about payments, e-commerce, and retail to help you succeed (with MONEI as your payments partner, of course).